Daily Pulse · · 08:30 CET · framework · ROK

Rockwell Automation is starting to look like one of the more interesting second-wave AI stocks — not because it makes GPUs, and not because it runs cloud models, but because it sits in the physical AI layer where AI meets the real economy.

ROK is interesting because it sits at the intersection of where AI increasingly goes next: factories, warehouses, data centers, semiconductor facilities, energy infrastructure, robotics, motion control, machine control, industrial software and automated production lines. That is the physical AI layer. The first AI trade was about building the digital brain — GPUs, networking, cloud infrastructure, memory, data centers. One of the next trades is about connecting that intelligence to physical systems: controlling, optimising, simulating, monitoring and automating them.

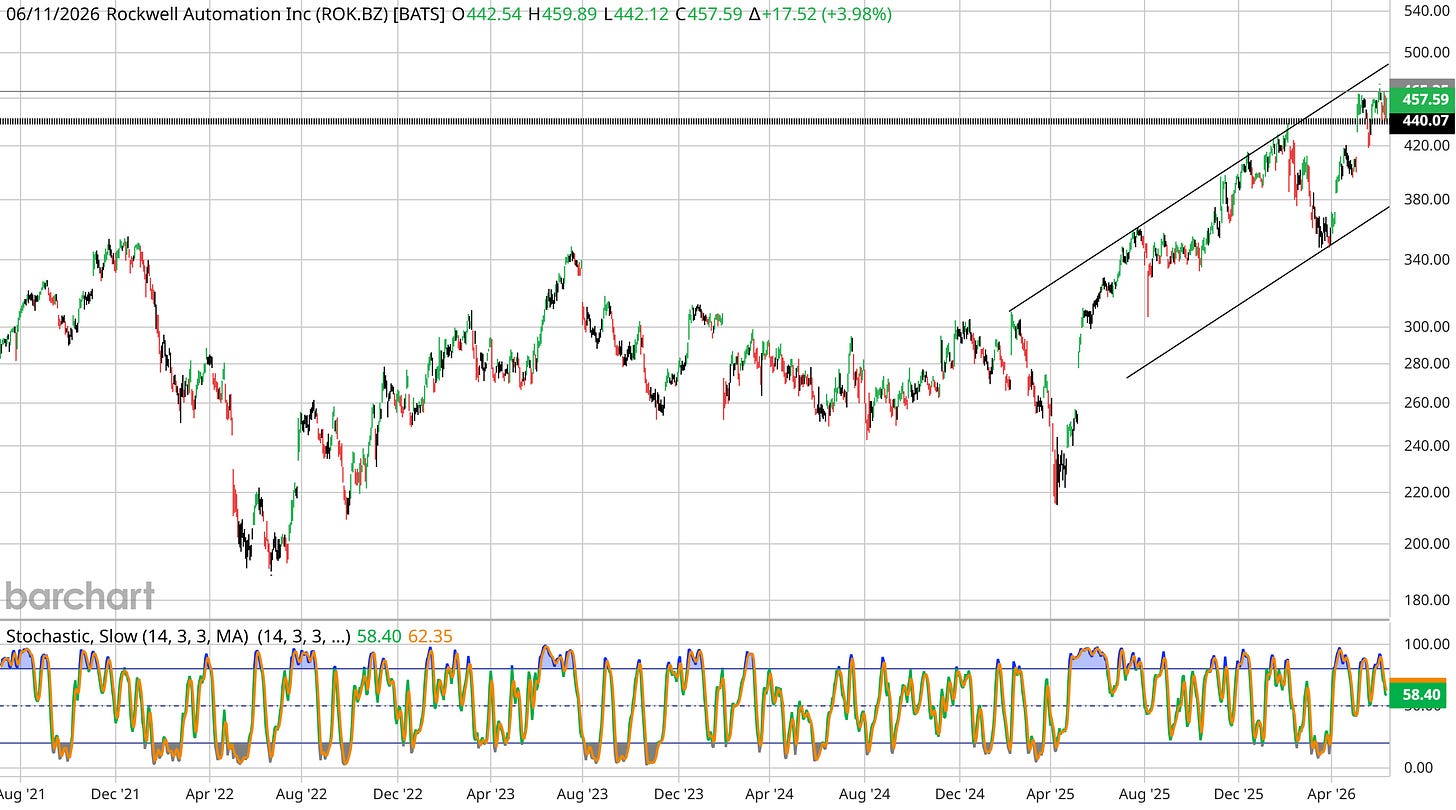

The chart is now confirming that investors are beginning to recognise the story. ROK has pushed above the key $440 resistance, closing near $457.59 after a strong session. The stock has been trending within a rising channel since spring 2025, and this latest move looks like a potential breakout from a longer consolidation zone.

What's the buzz?

Rockwell's latest quarter was meaningfully better than expected. In fiscal Q2 2026 the company reported sales of $2.24 billion, up 12% year over year, with organic sales up 9%. Adjusted EPS came in at $3.30, up 32% year over year, while enterprise operating margin expanded to 22.5%, up 350 basis points from a year earlier.

More important, management raised guidance. Rockwell now expects fiscal 2026 reported and organic sales growth of 5% to 9%, up from the prior range of 2% to 6%. It also raised adjusted EPS guidance to $12.50–$13.10, with the midpoint now around $12.80, about $1 higher than before. This is not a stock moving only on a theme — it is moving on stronger sales growth, higher margins, better earnings and stronger guidance.

C — free account

The free C account unlocks the full Daily Pulse — every section of this read.

One tap with Google or one email — no password, no card. You are signed in until you sign out, on this browser, from then on.

Join the Look — freeAlready joined on this browser? The full edition shows automatically — if it doesn't, sign in again here. Looking for the archive, portfolios and realtime? That is C+.